What Is a Temporary Buydown?

Instead of lowering your offer or asking price, please consider using a temporary 3-2-1, 2-1, 1-1 or 1-0 Seller Paid Buydown.

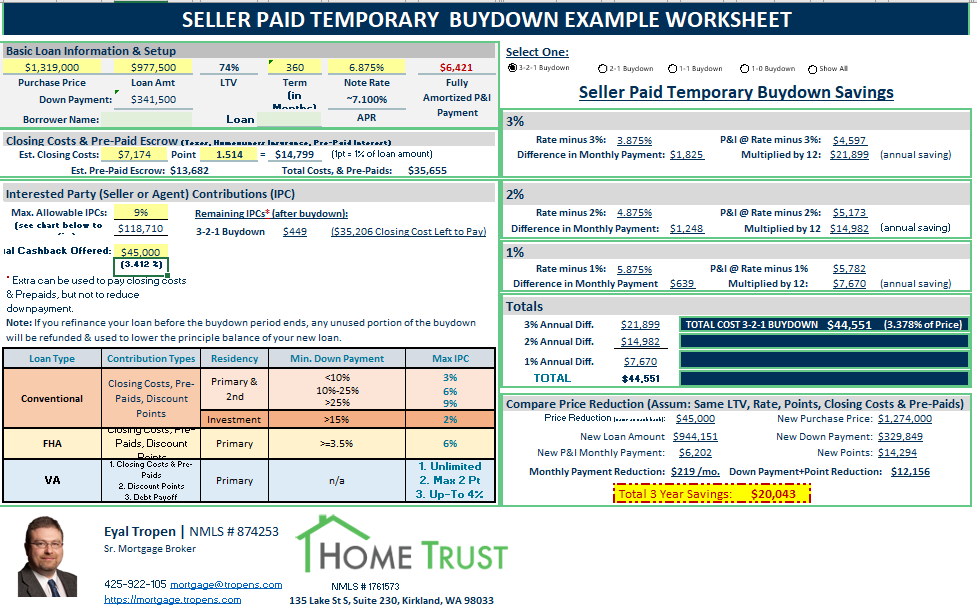

The seller will pay, at closing, a pre-set amount which will cause the buyer’s effective rate to be lowered in the first few years of the life of the loan.

- With a 3-2-1 buydown, the effective rate will be reduced by 3% during the 1st year, 2% during the 2nd year, and 1% during the 3rd year. Starting with the 4th year of the life of the loan, the rate will go back to the fully amortized loan rate.

- With a 2-1 buydown, the effective rate will be reduced by 2% during the 1st year, and 1% during the 2nd year. Starting with the 3rd year of the life of the loan, the rate will go back to the fully amortized loan rate.

- With a 1-1 buydown, the effective rate will be reduced by 1% during the first TWO years, then starting with the 3rd year of the life of the loan, the rate will go back to the fully amortized loan rate.

- With a 1-0 buydown, the effective rate will be reduced by 1% only during the 1st year. Starting with the 2nd year of the life of the loan, the rate will go back to the fully amortized loan rate.

How Does It Help Me?

This strategy is especially effective in periods when the prevailing mortgage interest rates are relatively high, and there is a reasonable expectation they will come down significantly during the buydown period (such as when inflation is high, but expected to cool down).

NOTE:

-

- Borrowers must qualify based on the fully amortized interest rate & payment which will apply after the temporary buydown ends.

- When you sell or refinance your home, any unused portion of the buydown will be applied as a principal reduction to your loan balance. Unlike paying points to permanently buydown the rate, this money is not lost!

- Some lenders limit Temporary Buydowns to Primary Residence Conventional Loans. Some extend to FHA & VA. Some allow even 2nd homes or Investments.

- Temporary buydown fees must be paid by the seller, with appropriate language in the purchase & sale agreement.

- The borrower may still pay additional points for a permanent rate buydown – ask your loan officer for details and a total cost analysis.

- Not all lenders offer Temporary Seller Paid Buydowns and some only offer a limited set of options, so your fully amortized, undiscounted interest rate may be higher than would be available otherwise.

Download Buydown Calculator