If you’re in the market for a mortgage, you may have heard rumblings about a new, unfair tax on those with higher credit scores.

Don’t panic and DEFINITELY don’t start intentionally lowering your credit score!

I’m here to help separate facts from fiction.

First and foremost, you will NEVER get a better deal on a mortgage if your credit score is lower. No matter what you read or saw online, there is NO scenario where someone with a lower credit score will pay a lower fee than someone with a higher credit score would on the same loan!

So what’s all the fuss about?

It all comes down to changes in Loan Level Price Adjustments (LLPA’s) imposed by Fannie Mae & Freddie Mac – the two entities that guarantee a vast majority of new mortgages. LLPA’s impact the interest rate & closing costs charged when obtaining a mortgage, and are set based on loan features such as your Credit Score and the Loan-To-Value (LTV) ratio.

In January of this year, the Federal Housing Finance Agency (FHFA) – the Federal Agency regulating FannieMae and FreddieMac, announced changes to LLPA’s, which are set to go into effect on loans delivered to the agencies on or after May 1st, 2023.

WAIT! What??? This is not something that just happened this weekend????

No, this is old news. The confusion arised because changes that impact fees and guidelines are almost always implemented based on the date the loan is “delivered” to Fannie/Freddie. “Delivery” usually occurs weeks, and sometimes months after the loan is closed. Most lenders already implemented these changes some time ago, starting with loans that were locked as early as February or March.

So, what is changing?

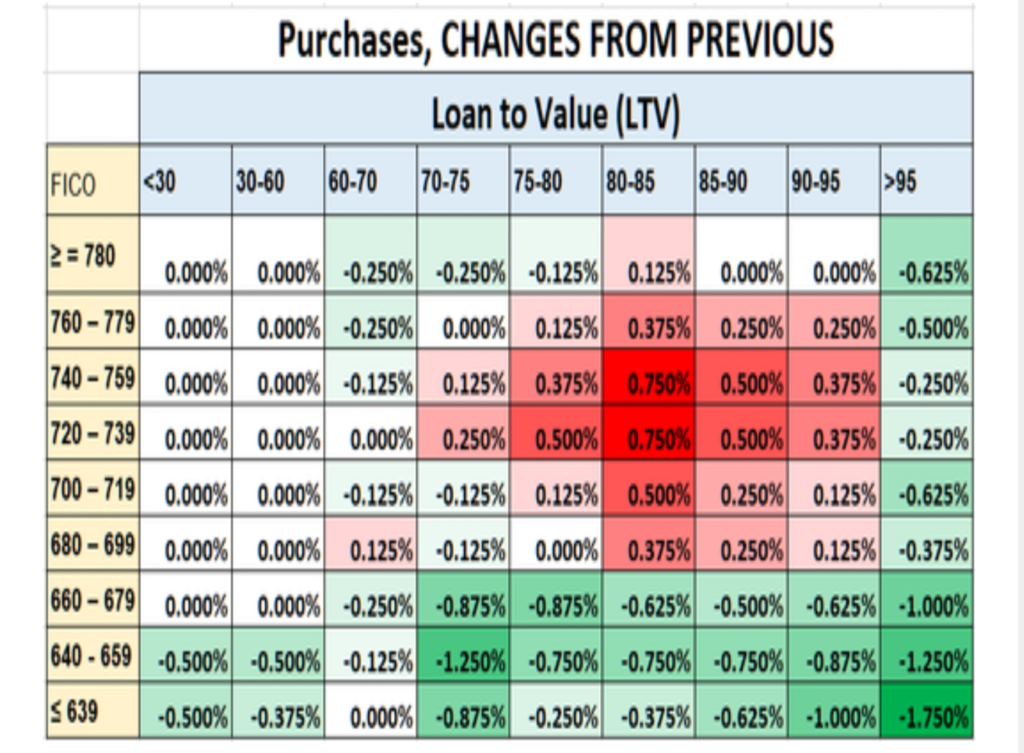

The fact is that LLPAs are indeed changing in a way that improves costs for those with lower credit scores and increases costs for those with higher credit scores, reducing the gap between the two, compared to what it was before.

However, there is NO scenario where these changes will cause someone with a higher credit score to have a higher fee than someone with a lower score.

The changes have upset many people, and the tables and charts that have been circulating online can be misleading.

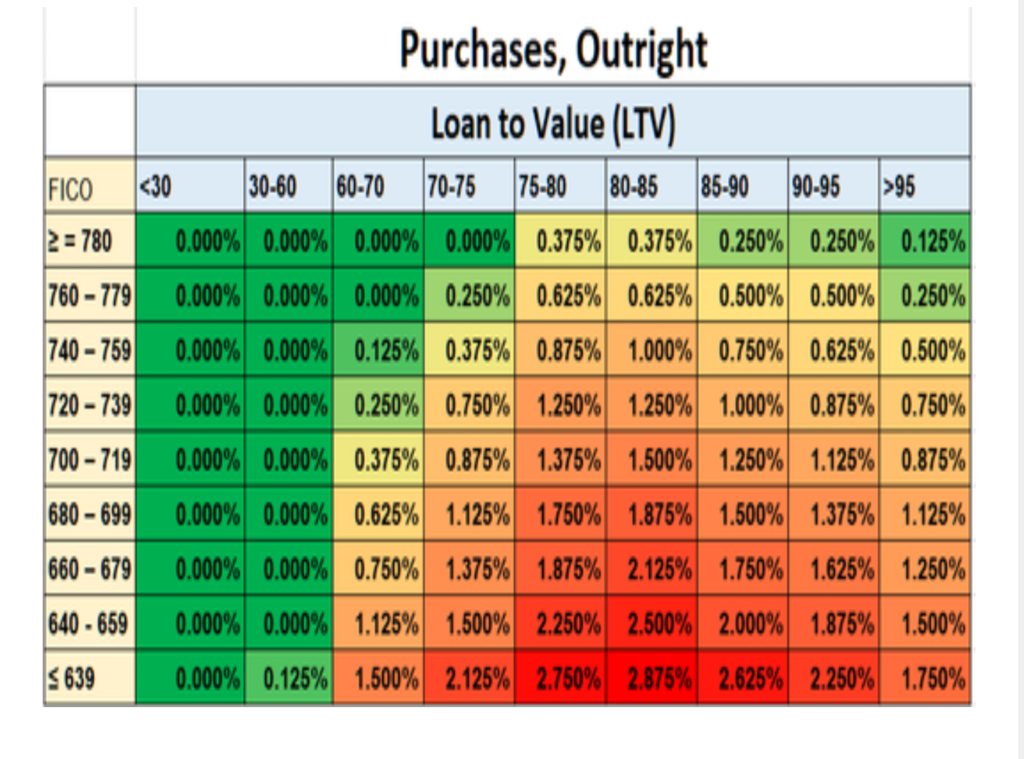

The differences in LLPAs before and after the changes show that costs are rising for those with higher credit scores and falling for those with lower credit scores. However, the outright LLPA chart below for the same matrix of credit scores and loan-to-value ratios clearly shows that those with lower credit scores will still pay significantly more than those with higher credit scores.

So why is this happening, and is it “Fair”?

FannieMae and FreddieMac through their regulator, the FHFA, charted a “mission” to promote affordable homeownership, and in their view, these changes are supposed to align with this mission.

While this change upsets many and draws a lot of criticism, views on this type of social justice can be subjective, and depend on one’s political, economic, and moral beliefs.

Pro-LLPA Change Perspective:

Some may argue that it is an act of social justice to provide support to individuals with bad credit who may not otherwise be able to afford housing. This perspective is based on the belief that everyone deserves access to affordable housing, regardless of their financial history. Advocates of this view may argue that various factors can contribute to bad credit, such as low income, job loss, medical issues, or systemic inequalities. By subsidizing mortgage loans for those with bad credit, the argument is that society can help address these underlying issues and promote a more equitable distribution of resources.

Anti-LLPA Change Perspective:

Others may argue that making people with good credit (who are not necessarily richer or more affluent than people with bad credit) subsidize mortgage loans for people with bad credit is an act of social injustice. This perspective contends that individuals should be held responsible for their financial choices and that burdening those with good credit is unfair, and could ultimately lead to a less stable financial system.

In Summary:

Whether you agree with these changes or not, they are here to stay and are already priced into your loan. Even with these fees, we’re seeing rate improvements from what they were a few months ago, and as Inflation gets under control we expect to see this trend continue.

If you want to find out how this affects you, and what mortgage you qualify for, start a loan application or give me a call today!